Page 131 - Annual Report 2020

P. 131

/ 126 QF CR A ANNU AL REP OR T 2020

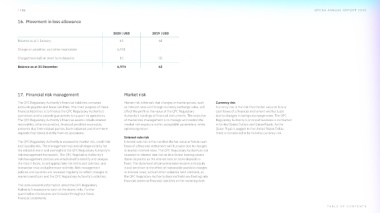

16. Movement in loss allowance

2020 | USD 2019 | USD

Balance as at 1 January 63 68

Charge on penalties and other receivables 6,901 -

Charge/(reversal) on short term deposits 10 (5)

Balance as at 31 December 6,974 63

17. Financial risk management Market risk

The QFC Regulatory Authority’s financial liabilities comprise Market risk is the risk that changes in market prices, such Currency risk

accounts payable and lease liabilities. The main purpose of these as interest rates and foreign currency exchange rates, will Currency risk is the risk that the fair value or future

financial liabilities is to finance the QFC Regulatory Authority’s affect the profit or the value of the QFC Regulatory cash flows of a financial instrument will fluctuate

operations and to provide guarantees to support its operations. Authority’s holdings of financial instruments. The objective due to changes in foreign exchange rates. The QFC

The QFC Regulatory Authority’s financial assets include interest of market risk management is to manage and control the Regulatory Authority’s principal business is conducted

receivables, other receivables, financial penalties receivable, market risk exposure within acceptable parameters, while in United States Dollars and Qatari Riyals. As the

amounts due from related parties, bank balances and short-term optimising return. Qatari Riyal is pegged to the United States Dollar,

deposits that derive directly from its operations. there is considered to be minimal currency risk.

Interest rate risk

The QFC Regulatory Authority is exposed to market risk, credit risk Interest rate risk is the risk that the fair value or future cash

and liquidity risk. The management has overall responsibility for flows of a financial instrument will fluctuate due to changes

the establishment and oversight of the QFC Regulatory Authority’s in market interest rates. The QFC Regulatory Authority is not

risk management framework. The QFC Regulatory Authority’s exposed to interest rate risk on its interest bearing assets

risk management policies are established to identify and analyse (bank deposits) as the interest rate on bank deposits is

the risks it faces, to set appropriate risk limits and controls, and fixed. The statement of comprehensive income and equity

to monitor risks and adherence to limits. Risk management is not sensitive to the effect of reasonable possible changes

policies and systems are reviewed regularly to reflect changes in in interest rates, with all other variables held constant, as

market conditions and the QFC Regulatory Authority’s activities. the QFC Regulatory Authority does not hold any floating rate

financial assets or financial liabilities at the reporting date.

This note presents information about the QFC Regulatory

Authority’s exposure to each of the above risks. Further

quantitative disclosures are included throughout these

financial statements.

T ABLE OF C ONTENT S